A longer version of this story originally appeared in ProPublica on Feb. 9.

At first glance, July 24, 2015, seems to have been a brutal trading day for Steve Ballmer, the former Microsoft CEO. He dumped hundreds of stocks, losing at least $28 million.

But this was no panicked sell-off. Among the stocks Ballmer sold were those of the Australian mining company BHP and the global oil giant Shell. Had Ballmer lost confidence in BHP’s management? Was he betting that the price of oil would not soon recover? Not at all. That very day, Ballmer also bought thousands of shares in BHP and Shell.

From the top:

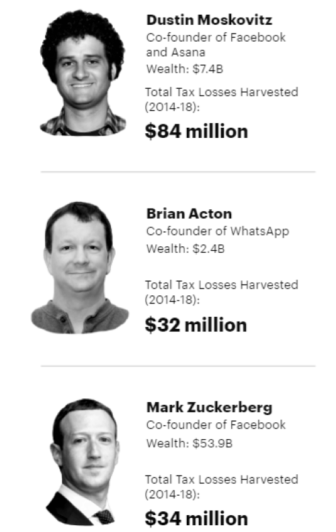

Dustin Moskovitz

Co-founder of Facebook and Asana

Wealth: $7.4B

Total Tax Losses Harvested (2014-18):

$84 million

Brian Acton

Co-founder of WhatsApp

Wealth: $2.4B

Total Tax Losses Harvested (2014-18):

$32 million

Mark Zuckerberg

Co-founder of Facebook

Wealth: $53.9B Total Tax Losses Harvested

(2014-18):

$34 million

Sources: Forbes, IRS data, ProPublica analysis

Why would he sell and buy shares in the same companies on the same day? The answer is counterintuitive to the average person but obvious to a sophisticated investor: A loss, for tax purposes, is valuable; a big one can wipe out millions in potential taxes. Ballmer’s two-step process allowed him to use the loss to lower his taxes, while the near-simultaneous purchase meant he effectively hadn’t changed his investment.

Since 1921, claiming tax losses from so-called wash sales — selling shares of a company then buying them again within a short period — has been forbidden. But Ballmer collected his losses anyway because, technically, the types of shares he bought and sold weren’t the same.

Both Shell and BHP offered two different versions of their common stock. For each company, the two stocks were legally distinct, but they performed very similarly because, after all, they were shares in the same company.

Ballmer’s not-so-bad day, in fact, was carefully planned, part of a strategy by Goldman Sachs, which conducted the trades on Ballmer’s behalf, to wield the stock market’s natural volatility to the billionaire’s advantage. At Goldman, the hundreds of stocks in Ballmer’s “Tax Advantaged Loss Harvesting” accounts were selected to follow the movement of the broader markets. Over time, the markets, as they had historically, would buoy Ballmer’s investments upward. When, inevitably, some of the stocks underperformed or the whole market dipped, Goldman was ready to pounce, selling off the losers and replacing them with equivalents.

Replacements were identical securities

Sometimes, the replacements were nearly identical securities, as with Shell and BHP. More often, they were not. But well-tuned software could easily find the right stocks to keep the accounts the bounce back.

Over and over, Ballmer sold and bought stocks in roughly equivalent amounts, as on that July day, when he swapped around $200 million worth. A month later, he did it again, landing at least $23 million in tax-reducing losses. Similar efforts that December brought $26 million more.

ProPublica estimates that from 2014 through 2018, Ballmer was able to generate tax losses totaling $579 million without changing his investment portfolio in a meaningful way. The tax savings from these losses amount to at least $138 million.

The scale of Goldman’s feat was remarkable, but Ballmer was just one client pursuing such a strategy. And Goldman was just part of an industry that helps the ultrawealthy report billions in losses — and save billions in potential taxes — even as their fortunes rise.

ProPublica was able to reconstruct the tax-loss strategies of scores of the nation’s wealthiest people, including Ballmer and Facebook co-founders Mark Zuckerberg and Dustin Moskovitz, using a trove of IRS data that has been the basis for “The Secret IRS Files” series. This trove includes not only some two decades of tax returns for thousands of the nation’s wealthiest citizens but also voluminous records of their trading.

After inquiries by ProPublica, Goldman said it would halt transactions like Ballmer’s Shell and BHP trades. Goldman conducted a review, according to a statement by the bank, and found that a “very small percentage” of its “tax investment solutions” trades were “inadvertently made in a manner inconsistent with our strategy.” The bank said it strives “to provide best-in-class investment advice to clients, consistent with both the letter and the spirit of all applicable tax laws and regulations.”

A Ballmer spokesperson said: “Steve takes his responsibility to pay taxes very seriously. Goldman Sachs has just provided Steve with corrected loss reporting information for prior years. Steve will amend his filings and pay any associated tax, interest or penalty promptly.”

But, by Goldman’s own description, it is halting only a narrow slice of its loss-generating trades — the ones involving two kinds of stock from the same company.

Laws are toothless

Goldman’s ability to deliver tax losses to its clients won’t be significantly curtailed. That’s because over the past 25 years, investing has undergone a transformation that’s made the law against wash sales toothless. Improved computing, new financial products, cheaper trading costs and a shift away from picking stocks to passively tracking the broader market are the main ingredients of the change.

Asset managers have used these advances to forge loss-harvesting accounts that boast hundreds of billions of dollars in assets. What the law sought to prevent — generating a tax loss without a substantial change in the investment — is now commonplace.

That ability is available even for small-time investors, who can mimic the sorts of techniques used by Goldman on their own or opt for products offered by mass-market brokerages such as Vanguard and Charles Schwab. But relatively few Americans have stocks or mutual funds outside of tax-protected retirement accounts, meaning most can’t employ the strategy.

It is the wealthiest who benefit most. The losses can be used to erase an unlimited amount of investment gains. Someone like Ballmer can easily deploy $100 million in losses to cancel out a $100 million gain from selling some of his vast Microsoft holdings. It’s a very different story when it comes to wages and other forms of income, of which only $3,000 can be offset. On average, only the top 0.001% of taxpayers made a majority of their income through investment gains in 2018, according to public IRS data.

Those gains, like many aspects of wealthy Americans’ tax returns, are usually the result of careful planning. Since, in the U.S. system, gains aren’t taxed until they’re sold, even the richest Americans can have years where they owe no tax at all.

The story is exactly the opposite with investment losses. From 2014 to 2018, Ballmer grew $22 billion richer, a fact that doesn’t appear on his tax returns. Meanwhile, Goldman made sure that even momentary losses were listed by the thousands.

High-income clients pick their losses

For the rich, the “tax system is sort of like a rigged coin,” said David Schizer, a tax expert and professor at Columbia Law School: “If you win, you get to keep all of it, but if you lose, you can pass some of those losses on to the government.” The wash sale rule, he said, is easily skirted by “well-advised taxpayers.”

IRS data shows how widespread the use of investment losses is among the richest Americans. In the U.S., short-term gains, those sold less than a year after buying, are taxed at about twice the rate (around 40% for the top bracket) as long-term gains. That makes short-term losses more valuable since they reduce this higher tax rate income. In 2018, almost two-thirds of Americans with income over $10 million reported net short-term losses. That was the highest share of any income slice; with more income, counterintuitively, came more losses — at least, on their taxes. Meanwhile, long-term losses were rare for them.

Take a look at the taxes of Jim Walton, the youngest son of Walmart founder Sam Walton and the 10th-wealthiest American, and you’ll see years of short-term losses, thanks to a tax-loss harvesting account at Northern Trust, a bank that specializes in managing the assets of the rich. (A representative for Walton declined to comment.)

Losses meant riches for Walton

From 2014 to 2018, Walton grew $10 billion richer, according to Forbes, but reported only $111 million in long-term gains on his taxes. Since his losses easily overwhelmed those gains, he paid no taxes on them at all.

In November 1920, a reader of The Wall Street Journal identified as R.H.T. wrote in with a question. It was a time with parallels to today: The stock market, after reaching highs amid a pandemic (then the Spanish flu), had plummeted. R.H.T.’s portfolio had fallen about $50,000 ($750,000 in current dollars).

“I do not want to sell these stocks at the present market,” wrote R.H.T. “Would it be legal for me to sell these stocks and deduct the loss from this year’s income, even though I bought them in again the same day?” Yes, the Journal responded, the transaction was permitted under the law.

“Basically, the strategy went viral,” said Lawrence Zelenak, a law professor at Duke Law School, and author of a history of the early income tax.

Lawmakers decided to do something about “evasion through the medium of wash sales,” as a 1921 Senate conference report put it. They passed a law that barred taking a tax deduction if, within either 30 days before or 30 days after a sale, an investor bought a security that was “substantially identical” to the one sold.

In the following decades, investors still found ways to collect losses that would reduce their taxes. Often, the volume of selling at year-end was enough to temporarily depress stock prices.

But with the wash sale rule in effect, there were real risks to what was often known as “tax-loss selling.” Investors could sell their losers and try to pick stocks with better prospects.

That, as The New York Times reported in 1983, often led to “regret” when an abandoned stock went to the moon. If investors wanted to stick with a stock, they’d have to work around the 60-day limitation. That meant either buying the same stock 30 days before they sold (called “doubling up”) or after. Both options carried danger. If the stock continued to tank while they were doubled up, their losses were compounded, and if the stock boomed before they could buy back in, they missed out.

New strategies for the super rich

In the mid-1990s, amid a historic market ascent, new strategies were forged to serve a new generation of super rich Americans. Asset managers began to emphasize post-tax returns. “Tax-aware investing is the challenge of the moment,” wrote Jean Brunel, the chief investment officer of JP Morgan’s global private bank, in the journal Trusts and Estates in 1997. The “tax-sheltering volatility” of stock movements, he explained, presented a “free option” to investment managers, who should “make a greater effort to identify ‘harvestable’ tax losses.”

Enabling this new “tax-loss harvesting” was a shift away from stock picking and toward passive products, such as funds that track the S&P 500. The wash sale rule still foreclosed easy solutions to the problem of replacing a specific stock. But replacing an investment in something as broad as the S&P 500 with another similar product became increasingly simple. As the Times reported in 1998, “it is getting easier for investors to find a close double for almost any portfolio.”

Exchange-traded funds, or ETFs, which emerged in the ’90s, fit this purpose perfectly. Unlike mutual funds, they could be traded like stocks, making them easier to use in loss-harvesting transactions.

Consider a trade by one billionaire in the summer of 2015. Markets had dropped after troubles in the Chinese economy, providing a loss-harvesting opportunity for investors with exposure to Asia.

Brian Acton of WhatsApp

Brian Acton, a co-founder of WhatsApp, which a year before had been sold to Facebook for $19 billion, was one of those investors. He owned shares of Vanguard’s emerging markets ETF, which tracks an index of companies in China and elsewhere.

At the end of August 2015, according to ProPublica’s IRS data, Acton sold $17 million in shares, resulting in a loss of $2.9 million. The same day, he bought $17 million worth of the emerging markets ETF offered by Blackrock.

The two funds have only minor differences, with large holdings in many of the same Chinese companies. Unsurprisingly, the two funds perform similarly.

When emerging markets fell even further toward the end of the year, Acton did the same deal in reverse: He sold Blackrock and bought back into Vanguard. That allowed him to bank another $600,000 in tax losses.

In 2015, well over 100 wealthy Americans in ProPublica’s database switched from one company’s emerging markets ETF to another to collect tax losses.

Asked about loss-harvesting transactions, Acton told ProPublica, “To be honest I’m not really aware of any events like that.”

“Broadly my wealth is managed by a wealth management firm and they manage all the day to day transactions,” Acton, who has donated to ProPublica, added in a brief exchange over the messaging app Signal, where he is now interim CEO. He did not respond to a detailed list of questions.

Why was Acton’s trade, and the many others like it, not a wash sale?

In theory, the stocks inside two different funds could overlap so much that the IRS might deem them “substantially identical” and thus disallow any tax loss on such a trade.

In practice, however, there is only one scenario in which the wash sale rule is consistently enforced. IRS regulations require brokerages to mark a trade as a wash sale if, in the 60-day period around the sale, the investor buys, in the exact same account, the exact same security (with the same ID, called a CUSIP number). The amount of the forbidden loss is then noted on a form, called a 1099-B, that brokerages send to the IRS each year to detail stock trades.

IRS offers no clear guidelines

Beyond that, the IRS has provided no clear guidelines. Instead, the agency has commented on only a few little-used scenarios, while directing taxpayers to “consider all the facts and circumstances” of a trade. Is it OK to swap Vanguard’s ETF tracking the S&P 500 for Blackrock’s version of the same index? Some tax experts say yes, some say no. Besides the IRS’ vague guidance, there are few relevant court cases, and all are decades old. (The IRS declined to comment.)

ProPublica’s analysis of its IRS data found dozens of examples of taxpayers switching between funds with the exact same holdings. More common were switches like Acton’s between funds with significant, but incomplete, overlap.

The clearest sign that these sorts of trades do not, in the IRS’ eyes, violate the wash sale rule is that ProPublica could find no example of the agency challenging one.

In fact, audits very rarely target wash sales at all, attorneys who’ve represented wealthy taxpayers in IRS disputes told ProPublica. “I have had only one audit on this,” said Bryan Skarlatos, a partner with Kostelanetz & Fink, and it was “for a trader who totally screwed up.”

As popular as ETFs are for harvesting losses, the premier vehicle for delivering tax losses to wealthy clients is another innovation of the 1990s: the separately managed account.

In these accounts, managers make decisions about what to buy as they would for a fund, but the investor owns the stocks directly. When the account mimics an index like the S&P 500, it’s called direct indexing.

Shell and BHP, both part of Ballmer’s loss-harvesting trade in 2015, each offered shares based in two different countries. Each company viewed these two versions as interchangeable in value. In fact, in 2022, both companies chose to merge their two classes into a single stock on a 1:1 basis.

ProPublica’s IRS data contained several hundred examples of these kinds of trades by Goldman clients dating back as long as 10 years ago. The records show instances of these sorts of trades through other brokerages, but the overwhelming majority were made through Goldman.

Goldman said that the impact of the now-halted trades on its clients would be “minimal,” and that it would “cover any costs they incur” as a result of disallowed losses. “We have also initiated a discussion with the IRS and will address any questions they may have on this matter,” the statement said. Generally, only returns filed within the past three years would be subject to possible audit.

At wealth management firms, loss harvesting accounts are often designed to work in tandem with other services, as a kind of knob to turn up or down, depending on the need.

At Iconiq Capital, this is part of an approach that goes far beyond investing to things like managing personal staff. In 2007, the firm’s co-founder, a former Goldman Sachs and Morgan Stanley banker named Divesh Makan, told a wealth management magazine that he’d even organized clients’ parties and helped find possible marriage partners. Clients, he said, “want us to look after them these days.”

Facebook’s Dustin Moscovitz

The San Francisco-based firm manages about $13.2 billion for its 337 high-net-worth clients, according to a regulatory filing. Among them is Facebook co-founder Moskovitz, Zuckerberg’s old roommate at Harvard. Since the mid-2000s, when Moscovitz’s six-figure Facebook salary made up almost all his income — he’s now worth more than $7 billion — his financial life has grown considerably more complicated. After leaving Facebook, Moskovitz co-founded Asana, a software company, in 2009, but his stake in Facebook still accounted for the vast majority of his wealth. He set about changing that. From 2012 through 2018, he sold $3.6 billion worth of his stock, funds that he, with Iconiq’s help, could then use for other investments.

One of those new ventures was a tax-loss generating account. In late 2012, Moskovitz harvested his first tax losses, according to ProPublica’s analysis. It was a tiny haul by the standards of a billionaire, just $309,000, but it was a start. By 2013, he’d put over $100 million into the account, and his tax losses began to swell. In December of that year, he sold off 153 stocks to produce his first million-dollar loss.

Asset managers recommend adding to a direct indexing account over time, since it ensures there are always new losses to harvest. That’s the strategy Moskovitz followed, every few months seeding $13 million here, $25 million there. As the account grew, so did the tax losses.

Although ProPublica could not determine which index Moskovitz’s account tracked, the transactions followed the telltale pattern of direct indexing. In March 2016, for instance, Moskovitz sold off a basket of 85 stocks worth $27 million and bought a collection worth about the same amount. The two baskets were stuffed with stocks that had performed very similarly in the previous year, according to ProPublica’s analysis. The trade delivered $6.2 million in losses.

Meanwhile, Iconiq arranged other investments for Moskovitz, and the point of these was simply to make money. Most of the money Iconiq manages is in the form of venture capital, private equity and hedge funds, and Moskovitz bought large shares of partnerships run by the firm with names like Iconiq Strategic Partners and Iconiq Access. From 2014 to 2018, Iconiq entities sent over $200 million to Moskovitz.

The two types of investments were complementary, with the direct indexing account helping to blunt the tax sting from that income. Over the same period, Moskovitz’s dozens of loss-harvesting trades resulted in $84 million in tax losses. That saved him at least $20 million in taxes, ProPublica estimates.

Mark Zuckerberg loses, then wins

For Zuckerberg, too, Iconiq provided the same twin services of providing and erasing income. His Iconiq investments earned him $88 million during the five-year period, while his tax-loss harvesting trades produced losses of $34 million.

Representatives for Iconiq and Moskovitz, who has tweeted that he’s “in favor of raising taxes on the wealthy,” did not respond to written questions. A representative for Zuckerberg said, “Mark has always paid the taxes he is required to pay.”

To prevent the wealthy from easily skirting the wash sale rule, Congress would need to change the law, experts said. One fundamental, but long-shot, reform would be to automatically tax the annual fluctuations of investments’ value (called “marking to market”). That would prevent the wealthy from being able to defer taxes on gains forever — and also render tax-loss harvesting unnecessary.

But even narrower changes could have an impact. Steve Rosenthal of the Tax Policy Center suggested a law aimed at how products like direct-indexing accounts are marketed: If an asset manager touted the ability to replace securities with positions that were economically the same, then those losses could be deemed wash sales. This, he said, wouldn’t be a major change, “but it might slow people down.”

Schizer, of Columbia Law School, suggested a more comprehensive reform: Congress should replace “substantially identical” with “substantially similar,” a phrase that is used in some other areas of tax law. That could rule out some of the most common harvesting moves, he said. The rule, he said, “ought to be updated to reflect how people invest today instead of how they invested 100 years ago.”

The Secret IRS Files

Inside the Tax Records of the .001%

Paul Kiel and Jeff Ernsthausen are reporters with ProPublica. ProPublica is a nonprofit newsroom that investigates abuses of power.

This story ought to be in The Wall Street Journal, but would anyone who reads it do anything about it?

Maybe Ro Khanna reads this paper and can team up with some Republicans and figure out how to change the tax law.

finally, the rubes are catching on

wealth is all about managing accounting losses – depreciation, wash-sales, carried interest, like kind exchanges – as tax destroys and accounting losses are the antidote to poisonous and corrosive nature of taxes

hopefully, the rubes will then realize the rich don’t pay taxes, certainly not like the rubes think. Not only do they have an array of ways to avoid taxes, but their income is made off assets (and the profit from those assets is extracted from the middle and working class) not their labor, so raising taxes only hurts the middle class who trade their lifeforce for crumbs and pay income and payroll taxes which provides the debt service on government over-spending

don’t worry your local uniparty masters see this and now are happy to extract lifefroce from the poor as well with sales tax, payroll tax, and gas tax

hopefully, the rubes will reach the next level when they realize almost every penny the government overspends eventually ends up in the pockets of the said rich – defense, SNAP, Section 8, LIHTC, Obamacare, to name a few… even a big chunk of the NGO spending on social workers ends up in landlords’ pockets.

one of the sneakiest sneaks in American history was the coining of the term “government waste” as if those dollars are lost in the bottom of the ocean or burnt in a pit in the back yard. Government waste directly ends up in the pockets of the rich and serves as a distraction to the rubes – convincing them that their Team Captains will put that waste to an end

and the rubes will transcend to be the enlightened when they realize that this overspend and outrageous waste recurs year on end (even with a bit of growth yoy) and can be securitized at valuations of 20-30x the annual profit it generates

remember it’s called capitalism, not whinerism nor laborism nor a debtors’/renters’ paradise – all cash flows are capitalized, mostly notably your subjugation

all of this explains the “right/left” divide, immigration, welfare, the defense budget, the uni-party that runs the federal government

the funniest thing I’ve ever heard was that welfare transferred wealth from the makers to the takers – which of course is only partially the opposite of the truth – welfare is the transfer of cash flows from the middle class to the rich, who then turn that into wealth as described above

but alas, the rubes will never realize this because they are too sure they are right, that their team is the true Righteous One, and they can’t see past their noses on how ridiculous and exploited they are. rubes will always be rubes as long as they hate each other

Great article. Losses and depreciation should just be dissolved from the tax code. They are the two biggest money makers for the rich.